Determining if an HVAC system is considered Qualified Improvement Property (QIP) is one of the most critical financial decisions a commercial property owner can make. Under the CARES Act of 2020, QIP was corrected to have a 15-year recovery period, making it eligible for Bonus Depreciation. However, not all HVAC work qualifies. To be considered QIP, the improvement must be made to the interior portion of an existing non-residential building and must be “placed in service” after the building was originally open for business.

The confusion often arises when distinguishing between QIP and Section 179 expensing. While Section 179 allows you to deduct the full cost of HVAC equipment (including rooftop units) up to a certain limit, QIP specifically looks at the internal infrastructure—such as ductwork, sensors, and interior air handlers. If your project involves a total system overhaul, understanding how to “bucket” these costs between QIP and standard capital improvements can be the difference between an immediate tax windfall and a 39-year depreciation slog.

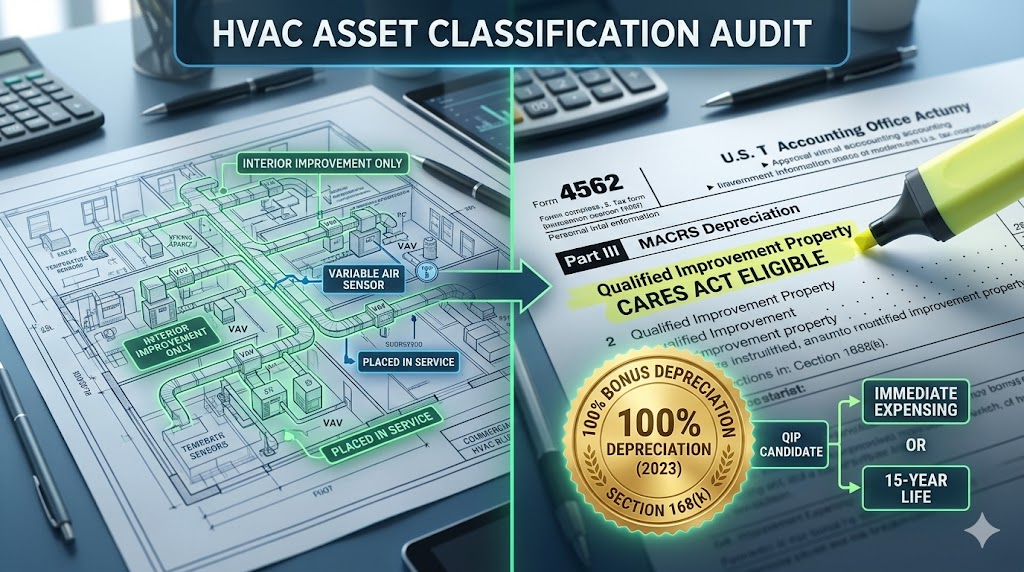

To see how your upcoming HVAC project should be classified for tax purposes, use the HVAC Tax Eligibility Auditor below.

What is Qualified Improved Property (QIP)

Qualified Improved Property is any improvement or upgrades made on the interior part of a building; provided that such building is classified as a nonresidential real property: in as much as the upgrade is placed in service after it has initially been placed in service by a taxpayer. The provision was included in the tax code as part of the 2015 law, to form the basic rulings for properties placed in service on the 1st of January 2016, or any day after.

For a proper understanding of the concept of QIP, a detailed explanation is provided about the key terminologies used in the definition below.

Interior part: This implies that only changes made to the inner portion of the building are classified as QIP; every other improvement made on the exterior part like the facade, or roof is not considered as QIP. Also, any improvements or changes made on land that surrounds a building are not included.

Non-residential: A non-residential building is a structure that is not occupied by a particular person or a group of persons. Such properties can be owned by an individual or group of people but it is not a permanent dwelling place for anybody. Examples of non-residential buildings include hospitals, prisons, empty plots of land, offices, shops, factories e.t.c. Improvements made on these buildings are qualified to be QIP.

On the other hand, any improvement made on residential buildings is not considered as a qualified improvement property. A residential building is any building that offers half of its total floor areas as a dwelling place. This includes Private houses, hotels, dormitories, apartments, lodging houses e.t.c. likewise, any improvement made on nursing homes or multi-family properties is also not eligible to be QIP.

Real property: Real property comprises land including every other asset and non-assets that is attached to it as well as the ownership rights and the prerogative to possess, lease, sell, or use the land for personal use. In the Qualified Improvement Property, code section 1245 which includes 5-year life assets are ineligible to be a qualified improvement property. This is in total aberration of the popular belief that both a 5-year asset and QIP can be joined together and treated as one unit, and can therefore be said to be eligible for a 100% bonus.

Is electrical work qualified improvement property?

Yes, any electrical installations as long as they fall within the categories of items stated earlier, are eligible to be classified as qualified improvement property.

Does HVAC count as qualified improvement property

Yes, HVAC counts as qualified improvement property. Any improvement made on building systems is considered to be an improvement to the whole building.

Therefore, Heating, ventilation, and air conditioning are eligible to be a Qualified improvement property. This also includes motors, compressors, pipes, chillers, furnaces, boilers radiators, and ducts.

💡 Pro Diagnostic Tip: Upgrading your building’s “brain” is one of the clearest paths to a QIP deduction. Adding a JACE Building Controller constitutes an interior improvement to an existing building’s mechanical system, which typically qualifies for 15-year depreciation and bonus expensing.

Can you section 179 an air condition rental property?

Yes, air-conditional for rental property is deductible under section 179. Section 179 provides that the cost of certain properties can be deducted by taxpayers in as much as the property has been placed in service.

The provisions of the section include tangible personal properties like machines and equipment purchased for business purposes. As a taxpayer, you can elect that the deductions be used as qualified real property.

Does CA allow section 179?

No, California does not allow the new alteration to section 179. However, exceptions were made for corporate entities or individual taxpayers to deduct $25000. Also if the property placed in service is worth more than $200000, the amount will be reduced.

Cares act qualified improvement property HVAC

The cares act also known as the Coronavirus Aid, Relief, and Economic Security Act fixes errors associated with retails and also makes qualified improvement property (QIP) worthy of depreciation bonus.

The cares act provides that qualified improvement property should be treated as a 15 years property, thereby making it possible for taxpayers to request for 100% depreciation bonus on items eligible for QIP.

💡 Pro Diagnostic Tip: The complexity of tax classification is a major factor in the total “Lifecycle Cost” of a system. High-efficiency systems may have a higher sticker price, but when combined with QIP bonus depreciation, the net after-tax cost can be significantly lower. Read our breakdown on Why Air Source Heat Pumps are Expensive to see how tax incentives impact the long-term ROI.

The act also changed the ADS recovery period for QIP from 39 years to 20 years and also enacts that taxpayers must ensure that they carry out the improvement.

Bonus: Sometimes, you might be making some changes to your property, but such changes wouldn’t be eligible for QIP. This will be the case if you are just repairing and not making any improvement on the property. As a result, you might want to know;

What are the differences between repairs and Improvement?

Repairs

- Cementing a cracked foundation.

- Changing clogged filter of your HVAC system or fixing the broken fan of your AC unit.

- Replacing of fixing a broken camera.

- Mending leaking roofs.

- Replacing of fixing a broken cabinet door.

Improvement

- Replacing old doors with new ones.

- Installing New floor.

- Changing the entire roof.

- Kitchen remodeling.

- Connecting central air conditioner to your building.

- Constructing additional rooms or garage within your building.